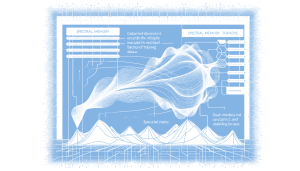

Spectral Memory introduces a novel mechanism that captures the hidden-state evolution across training mini-batches to encode temporal structures not available in individual sequences. By utilizing Karhunen–Loève decomposition, it extracts dominant modes and projects them into Spectral Memory Tokens, which provide global context and act as a structural regularizer for stabilizing long-range forecasting. This approach demonstrates competitive performance in time-series forecasting tasks, achieving low mean squared error (MSE) on datasets like ETTh1 and Exchange-Rate, and is designed to be easily integrated into existing systems. This matters because it offers an innovative way to enhance the accuracy and stability of predictive models by leveraging the training trajectory itself as a source of information.

Spectral Memory introduces a novel mechanism that captures the hidden-state evolution across training mini-batches to encode temporal structures not available in individual sequences. By utilizing Karhunen–Loève decomposition, it extracts dominant modes and projects them into Spectral Memory Tokens, which provide global context and act as a structural regularizer for stabilizing long-range forecasting. This approach demonstrates competitive performance in time-series forecasting tasks, achieving low mean squared error (MSE) on datasets like ETTh1 and Exchange-Rate, and is designed to be easily integrated into existing systems. This matters because it offers an innovative way to enhance the accuracy and stability of predictive models by leveraging the training trajectory itself as a source of information.